From Institutions to Infrastructure: Why Credit in Emerging Markets Demands a New Foundation

Summary

The transition from institutions to infrastructure represents a fundamental shift in how financial value is verified and settled.

WERITAS PERSPECTIVES · Infrastructure & Capital · April 2025 · 12 min read

The next trillion dollars of credit deployment in Sub-Saharan Africa will not be unlocked by adding more lenders. It will be unlocked by rebuilding the layer beneath them.

For decades, the dominant theory of financial inclusion has been institutional: build more banks, license more lenders, extend more branches. The logic was intuitive if access to credit is the problem, then more credit institutions should be the answer. Yet across Sub-Saharan Africa, formal credit penetration remains below 20% of GDP in most markets, informal lending still commands significant volumes, and the majority of creditworthy individuals have never received a formal credit decision at all.

Something deeper is broken and it is not the absence of willing lenders.

The gap is infrastructural. The rails on which credit moves identity verification, data interoperability, risk assessment, collateral anchoring, capital settlement were largely inherited from systems designed for different economies, different borrower profiles, and different data environments. The result is a compounding friction: institutions willing to lend cannot do so efficiently, borrowers with legitimate creditworthiness cannot be recognised at scale, and international capital cannot find its way to the precise risk exposures it seeks. The problem is not demand. It is architecture.

"The problem is not demand. It is architecture. The rails on which credit moves were designed for different economies, different borrowers, and a different data environment entirely."

The infrastructure deficit hiding in plain sight

Consider the practical journey of a credit decision in a tier-two East African market today. A borrower applies. The lender attempts to verify identity against fragmented registries. Credit bureau data, where it exists, reflects a narrow slice of formal-sector activity. Cash flow data from mobile money and informal commerce sits in siloed formats, incompatible with lenders' risk models. Collateral, often in the form of land, faces title ambiguities that take months to resolve. International capital providers, contemplating portfolio allocations to African credit, face an additional layer: currency risk, legal jurisdiction questions, and no standardised instrument through which to participate. A process that should take hours takes weeks, if it completes at all.

This is not a story of bad actors or regulatory failure. It is a story of missing infrastructure. The institutional layer exists; the plumbing beneath it does not.

| <20% | $330B+ | 3–5× |

| Formal credit penetration as share of GDP across most SSA markets | Estimated SME financing gap across Sub-Saharan Africa annually | Cost overhead added by fragmented identity and data verification |

Why institutions alone cannot solve this

The instinct, particularly among development finance institutions and impact investors, has been to respond with more capital at the institutional level credit facilities to MFIs, guarantees for bank lending, equity into fintech lenders. These interventions matter. But they treat a symptom rather than a cause. Each institution that receives this capital must still navigate the same broken infrastructure beneath it. The marginal cost of each credit decision remains high. The ability to reach thin-file borrowers at scale remains constrained. The capacity to connect local credit risk to international capital markets remains limited.

What is missing is a shared layer a set of protocols, standards, and instruments that any institution can build on, that any capital provider can price against, and that any borrower can be represented within. In other payments infrastructure, this insight has already transformed markets: the interoperability layer of mobile money rails reduced the cost of a P2P transfer in East Africa by an order of magnitude, not by adding more transfer agents, but by building shared plumbing. Credit has not yet had its equivalent moment.

"What is missing is a shared layer a set of protocols, standards, and instruments that any institution can build on, that any capital provider can price against, and that any borrower can be represented within."

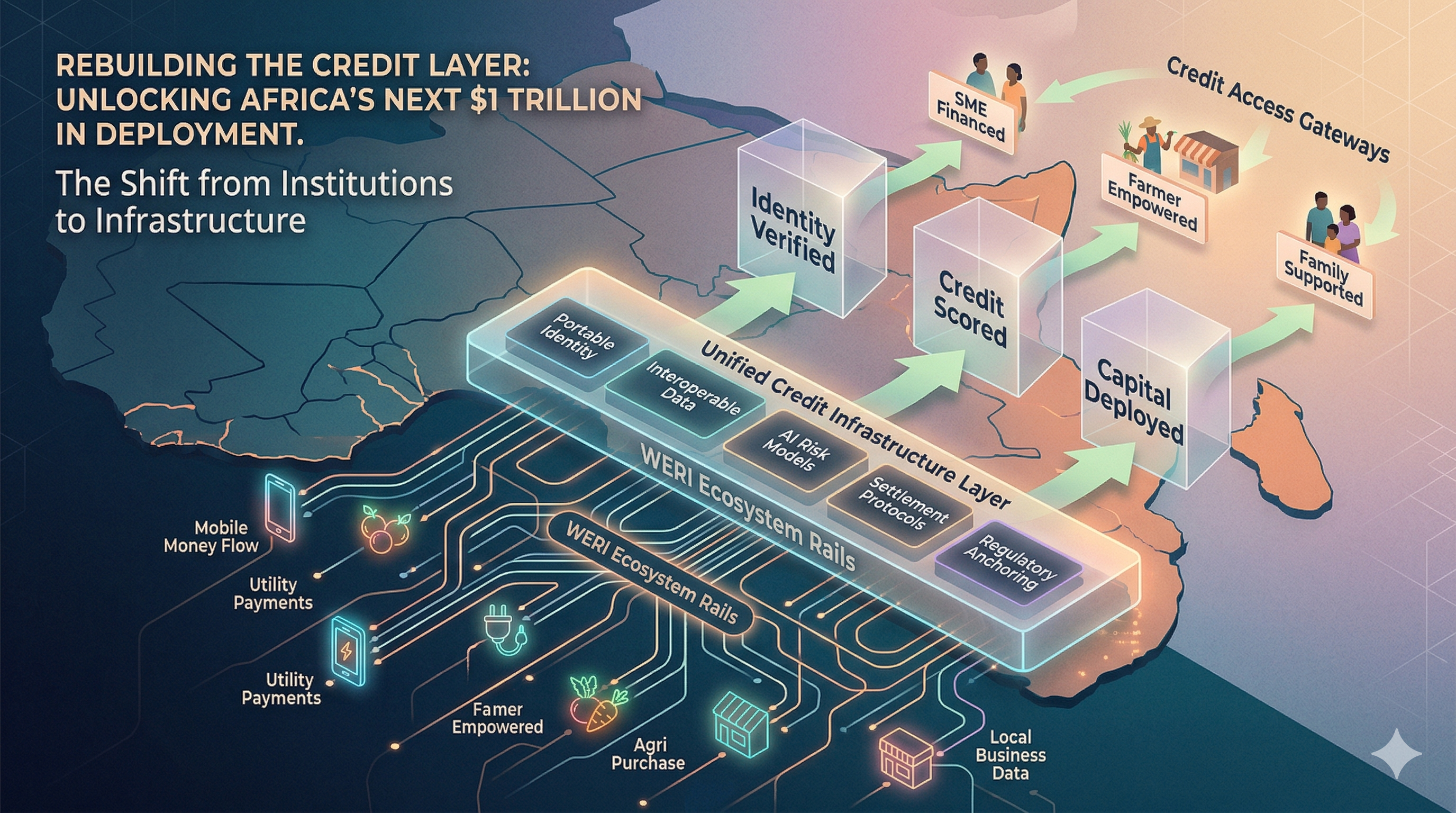

The components of a credit infrastructure layer

A genuine infrastructure layer for credit in emerging markets requires several interlocking components that today exist only in fragmentary or proprietary form.

Portable credit identity. Creditworthiness is not institution-specific a borrower who has demonstrated reliable repayment to one lender has produced a signal relevant to every future lender. Yet credit history today is largely trapped within individual institutions or narrow bureau ecosystems. A portable, privacy-preserving credit identity one the borrower controls and can present to any counterpart changes the economics of every subsequent credit interaction. Verification costs fall. Thin-file borrowers accumulate portable history. Competition for creditworthy borrowers intensifies, driving down rates.

Interoperable data and scoring. Alternative credit data mobile money flows, utility payments, agricultural purchase records, airtime top-up behaviour contains genuine predictive signal. The problem is not its absence but its inaccessibility. A true infrastructure layer standardises data access, normalises alternative data sources into credit models, and makes those models available as shared infrastructure rather than proprietary moats. Institutions compete on their relationships, their distribution, and their products not on their ability to access data that should be a shared input.

Structured credit instruments that travel. International capital has an appetite for emerging market credit exposure, but no standardised instrument through which to access it. Each transaction today requires bespoke legal structuring, jurisdiction specific documentation, and one off currency risk management. The result is that only the largest credit facilities can justify the overhead leaving vast segments of the market unreachable by global capital. Standardised credit instruments, structured at the infrastructure layer, reduce this friction and open new capital pathways to the full spectrum of credit assets in the market.

Regulatory anchoring and compliance rails. Infrastructure without regulatory legitimacy is architecture in isolation. A credit infrastructure layer must be built with local regulatory frameworks as a design constraint not an afterthought. Across East African markets where digital credit licensing and conduct standards are rapidly maturing, the infrastructure layer must demonstrate compliance by design: borrower protection, responsible lending mechanics, and transparent data governance baked into the protocol rather than bolted on by individual institutions.

Capital formation follows infrastructure

The relationship between infrastructure and capital is not coincidental it is causal. Mature capital markets exist where infrastructure is deep. Settlement infrastructure enables bond markets. Land registry quality predicts mortgage market depth. Payment rail standardisation drives consumer credit growth. In each case, the pattern is the same: infrastructure reduces the cost of each transaction, increases the legibility of risk, and enables new classes of capital to participate.

The inverse is equally true. Where infrastructure is shallow, capital is expensive, concentrated among a small number of participants, and structurally unable to reach the full depth of economic opportunity. This is not a failure of capital appetite it is a failure of the plumbing that would allow that appetite to be satisfied.

Emerging market credit is at an inflection point. The data substrate mobile penetration, digital payment adoption, formal identification systems has reached a threshold that makes a genuine infrastructure layer not only possible but necessary. The institutional appetite for deployment is present. The regulatory frameworks, while still maturing, are directionally aligned with infrastructure first approaches. What remains is the will to build the shared layer rather than continue to compete on proprietary verticals that, collectively, leave the market structurally underserved.

The Weritas thesis

Weritas was designed from the outset as an infrastructure project, not an institutional one. Our work is not to become another lender in an already crowded market; it is to build the credit rails on which the next generation of lenders, capital providers, and borrowers can operate more efficiently. The WERITAS ecosystem spanning portable credit identity via Web5 decentralised identity primitives, AI driven risk scoring anchored in interoperable data, and structured credit instruments that can be priced and traded by global capital is an attempt to instantiate this infrastructure layer in practice.

We have structured this deliberately: anchored in markets where digital credit regulation is most developed, built on licensed operational foundations that give us regulatory standing in market, and supported by institutional data partnerships that provide access to the alternative data signals necessary for thin file credit decisioning at scale. We are not building a proprietary moat. We are building shared plumbing and we are doing so in a way that is designed to be extended by the institutions, capital providers, and regulators who share an interest in a credit market that works for the full range of economic participants.

The shift from institutions to infrastructure is not a rejection of the institutional model. Institutions will remain the face of credit to borrowers, the relationship holders, the licensed operators. What changes is what they build on. And when the foundation changes, the scale of what is possible changes with it.

"We are not building a proprietary moat. We are building shared plumbing designed to be extended by the institutions, capital providers, and regulators who share an interest in a credit market that actually works."

The infrastructure thesis is ultimately an optimistic one. It holds that the barriers to financial inclusion in emerging markets are not inherent to those markets not a function of population characteristics, regulatory immaturity, or absence of entrepreneurial ambition but are structural artifacts of underinvestment in the shared layer. Address the infrastructure, and the institutional capacity to serve the market grows. Capital flows to risk it can see and price. Borrowers build histories that follow them. The feedback loops that deepen credit markets in developed economies become available to emerging ones.

The question is not whether this transition will happen. The data substrate, the regulatory direction, and the institutional appetite all point toward it. The question is whether it is built as a genuinely open infrastructure one that distributes the gains across the ecosystem or as a series of proprietary verticals that replicate the fragmentation at a different layer.

That choice, more than any individual product decision, will determine whether the next decade in African credit is one of incremental extension or transformative scale.

This perspective represents the views of the Weritas research team. It does not constitute investment advice or a solicitation of investment. · partners@weritas.io · www.weritas.io