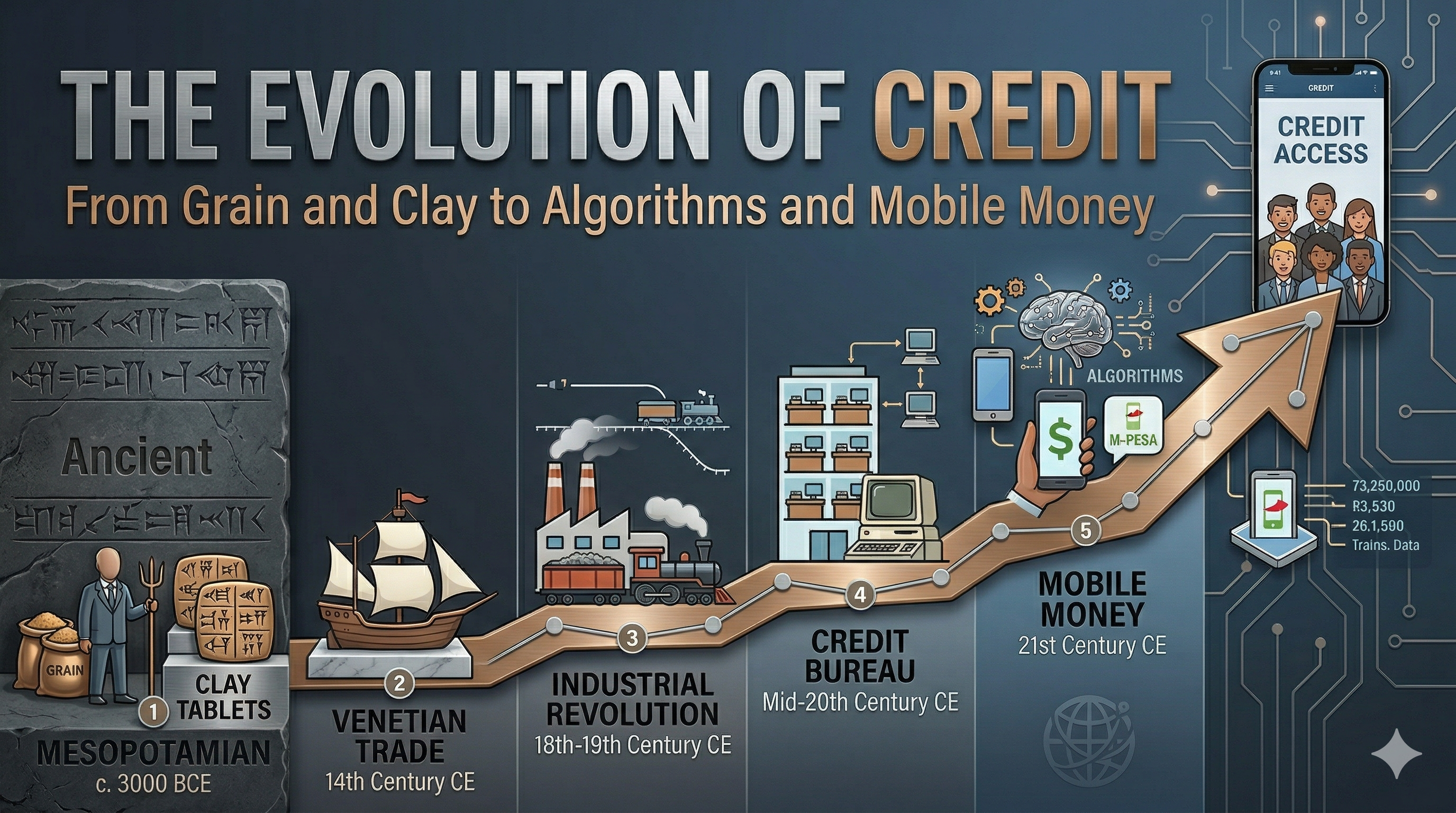

The Evolution of Credit: From Grain and Clay to Algorithms and Mobile Money

Summary

Traditional credit models rely on static, historical data that fails to capture real time economic potential.

WERITAS PERSPECTIVES · Capital & Markets · April 2025 · 16 min read

Credit is one of humanity's oldest inventions. It has financed every wave of civilisation from Sumerian harvests to Venetian merchant fleets to the industrial revolutions of the eighteenth and nineteenth centuries. And yet, for most of its five thousand year history, it has served the same narrow strata: those already known, already documented, already trusted. That is beginning to change. Understanding how we got here, and why the change is happening now, is essential to understanding what credit can become.

Part I: The long arc five thousand years in a grain ledger

The first recorded credit transaction did not involve a bank, a contract, or a credit score. It involved grain. Around 3000 BCE, in the city states of Mesopotamia Ur, Uruk, Nippur farmers who needed seed to plant the next season would borrow it from temple stores and repay it after harvest, with interest. The priests who managed those stores recorded every transaction on clay tablets: who borrowed, how much, what was owed, when it was due. Money lending can be traced to about 3000 BC in ancient Mesopotamia , and the system that emerged there was, in its essential structure, recognisable as credit.

What is remarkable about that system is not its antiquity but its sophistication. The Code of Hammurabi from ancient Mesopotamia reveals insights into sophisticated financial systems and regulations , including provisions that anticipated the concept of force majeure: if a storm destroyed a crop, the borrower was not required to repay that season. The debt tablet, in the remarkable phrase of the Code, could be "washed in water." The Babylonians, in other words, had already worked out that credit risk must account for events beyond the borrower's control an insight that modern credit modellers are still wrestling with in the design of climate sensitive lending products.

Food money in the shape of olives, dates, seeds or animals was lent out as early as c. 5000 BCE, if not earlier. Among the Mesopotamians, Hittites, Phoenicians and Egyptians, interest was legal and often fixed by the state. The principle that credit requires a recognised rate of return and that the state has a legitimate interest in setting the terms of that return is not a modern regulatory innovation. It is as old as organised agriculture.

The Greeks refined the Mesopotamian model. Following the invention of coinage in Lydia (present day Turkey) in the seventh or sixth centuries BC, the Greeks introduced private moneylenders and bankers known as trapezitai. Operating in public marketplaces called agoras, they initially focused on testing the validity of coins, but soon expanded into deposit taking, and providing loans at interest typically 12% per year for ordinary loans, with maritime loans carrying higher rates due to increased risk. The Greek contribution to credit was the introduction of risk pricing: maritime loans, which financed the dangerous passage across the Aegean and Mediterranean, commanded a premium because the probability of loss was higher. The principle of risk adjusted pricing, now embedded in every credit model in the world, was first articulated in the ports of Athens and Corinth.

The Romans systematised what the Greeks had pioneered. The Romans also implemented laws and regulations to govern banking activities, helping to standardise practices and protect both bankers and clients. Banking became integral to Roman commerce, supporting infrastructure projects, trade, and everyday financial transactions. Rome created the first professional class of financial intermediaries the argentarii whose function was not merely to lend but to guarantee, to settle, and to intermediate between parties who did not know each other. This was the beginning of the institutional trust that modern banking still depends on.

"Every era of economic expansion in human history has been preceded by an expansion of credit. The question has never been whether to extend it. It has always been how, to whom, and on what terms."

Part II: The medieval machinery of trade finance

The collapse of Rome did not end credit it merely relocated it. The medieval period saw the emergence of the instruments that would underpin European commerce for the next four centuries. Medieval trade fairs, such as the one in Hamburg, contributed to the growth of banking: moneychangers issued documents redeemable at other fairs, in exchange for hard currency. These documents could be cashed at another fair in a different country or at a future fair in the same location. These were, in embryonic form, letters of credit instruments of deferred payment that allowed merchants to conduct business across vast distances without carrying gold.

The Italian city states Florence, Venice, Genoa took this further. The Bardi and Peruzzi families dominated banking in 14th century Florence, establishing branches in many other parts of Europe. The most famous Italian bank was the Medici Bank, established by Giovanni Medici in 1397. The Medici did something that would not be truly replicated at scale for another six centuries: they built a credit network. Deposit money in Florence, draw on it in London. The branch banking system they created was the first mechanism for making credit portable for allowing the financial reputation built in one place to be honoured in another.

The collapse of the Bardi and Peruzzi banks in the 1340s brought down by the English crown's default on its sovereign debts was one of the first recorded systemic credit crises in history. The lesson was stark: even sophisticated credit institutions could be destroyed by concentrated sovereign risk. It is a lesson that has been learned and forgotten repeatedly in the centuries since, most recently in the sovereign debt crises of the 2010s.

By the seventeenth and eighteenth centuries, the tools of credit had proliferated. European colonial companies, such as the British East India Company and the Dutch East India Company, relied heavily on letters of credit issued by European banks to finance their global operations. The bill of exchange a written order to pay a specified sum on a future date became the engine of global trade, allowing the proceeds of spice sales in Amsterdam to finance the purchase of textiles in Bengal. Credit, in other words, had become the mechanism by which time and distance were collapsed in commerce. It had also, in the hands of colonial trading companies, become a mechanism for extracting value from the periphery to the centre a dynamic whose legacies are still visible in the structure of global capital markets today.

Part III: Industrialisation, bureaux, and the birth of the score

The Industrial Revolution created a credit problem that the personal, relationship based systems of the past could not solve. Manufacturing required capital on a scale that exceeded any individual merchant's capacity to assess. Workers moving from rural to urban settings needed credit instruments for housing, for consumer goods, for small business that did not depend on the personal knowledge of a local lender.

The response was institutional. In the early 19th century, the proliferation of retail credit led to the formation of numerous local credit bureaux. These entities gathered information from department stores and other retailers, sharing data about consumers' payment histories. By the 1960s, the United States alone had more than 2,000 such bureaux. The information they collected was, by modern standards, alarming in its breadth creditworthiness assessments that included personal character, marital status, racial background, and social reputation. The transition from personal judgement to institutional data represented progress in one sense it enabled scale but it replicated and, in many cases, amplified the exclusions of the personal system it replaced.

The decisive shift came in 1989. The 1989 debut marked the first nationwide, statistically driven FICO score available to lenders. Before then, lenders relied on manual underwriting and proprietary models rather than a single, uniform numeric model. Bill Fair and Earl Isaac's three digit score did something genuinely radical: it translated the subjective, personal, often biased assessment of creditworthiness into a single portable number that a lender in any city could read and act upon. Credit decisions that had taken days sometimes weeks could now take minutes. The democratisation of credit that followed in the United States through the 1990s was substantially enabled by this single instrument.

And yet the FICO score, for all its transformative impact in mature markets, was built on a foundation that only mature markets possessed: a dense ecosystem of bureau data, covering the formal credit interactions of a population that was already, in large part, banked. Export that model to a market where bureau coverage is thin, where formal credit history is sparse, and where millions of economically active adults have never had a credit card or a mortgage and the three digit number tells you very little. Today the bureau credit score is widely used to make lending decisions in developed markets across the world, but the scores are plagued by problems due to inaccurate or incomplete data. Without traditional credit history, these people won't have a good credit score and financial institutions have no way of assessing risk.

This is the structural gap that defines emerging market credit: not the absence of creditworthy borrowers, but the absence of the infrastructure to see them.

Part IV: The mobile money revolution credit finds a new rail

The story of credit in the twenty first century is, in large part, the story of mobile money. It began on the east coast of Africa.

M-Pesa launched in Kenya in 2007 not as a credit product, but as a simple person to person money transfer service. Its designer, Vodafone engineer Nick Hughes, described the vision plainly: make it possible to send money home using a mobile phone, eliminating the informal networks of cash couriers and matatus that served as Kenya's de facto remittance system. The uptake was faster than anyone had projected. Within a decade, M-Pesa had become something more consequential than a payments service. By 2023, M-Pesa boasted over 51 million active users, handling transactions valued at more than $50 billion annually almost a quarter of Kenya's GDP. The service had become, in effect, a financial infrastructure for an entire nation.

What M-Pesa created, beyond a payments channel, was data. Every transaction every school fee payment, every market purchase, every airtime top up was logged, timestamped, and associated with a SIM card. For the first time in Kenya's history, it was possible to construct something approximating a cash flow record for individuals who had never held a bank account and who would register as invisible on any credit bureau's screen. The credit implication was not immediately obvious, but it was profound: here was a dataset that could answer the question a lender most needed answered does this person manage money responsibly?

The answer, when examined at scale, was yes. Hundreds of thousands of Kenyans whose borrowing potential would have been invisible to a traditional bank turned out to be reliable credit risks when assessed against their mobile money behaviour. The credit products that emerged from this insight from M-Shwari to Tala to Branch demonstrated that it was possible to originate, disburse, and recover small ticket loans entirely through mobile infrastructure, with underwriting models built on transaction data rather than bureau files.

The scale that followed was continental. Africa now dominates mobile money, processing 74% of global transactions $1.1 trillion in 2024 alone. Mobile money platforms are transforming financial access, with over 1.1 billion registered accounts and growing services like micro lending, insurance, and cross border payments. Uganda stands out for a remarkable statistic: mobile money transactions now represent 94% of its GDP. In Nigeria, instant payments infrastructure processed over $1 trillion in transactions in 2024 , while BNPL markets valued at $15.5 billion across Africa and the Middle East in 2024 are projected to reach $33 billion by 2029.

"Mobile money did not just provide a new channel for credit. It created, for the first time, a real time record of economic behaviour for populations that traditional credit infrastructure had never been able to see."

The broader global data tells the same story of acceleration. According to the World Bank Group's Global Findex 2025 report, 79% of adults globally now have an account either at a bank or similar financial institution or through a mobile money provider. Low and middle income economies saw much steeper gains, with financial account ownership climbing 33 points from 42% in 2011 to 75% in 2024 a staggering 80% increase. The biggest increases occurred in Senegal and the Kyrgyz Republic, where account ownership surged 70 points between 2011 and 2024. In Sub Saharan Africa, 40% of adults had a mobile money account in 2024, up from 27% in 2021.

But the World Bank's data also contain a warning: only about a quarter of adults in low and middle income economies used formal credit in 2024. An additional 35% relied on informal sources such as family or friends. The account has arrived; the credit has not. The gap between financial account ownership and formal credit access is the defining challenge of the next decade.

Part V: India's infrastructure model credit through public rails

The most ambitious experiment in credit infrastructure transformation currently underway is not in Africa. It is in India.

India Stack the government led digital infrastructure project comprising Aadhaar (biometric identity), Jan Dhan (universal bank accounts), and UPI (instant payments) represents a deliberate attempt to build the preconditions for mass credit access through public infrastructure rather than commercial intermediation. The scale of what has been achieved is genuinely without precedent in economic history.

With more than 530 million bank accounts opened under the Pradhan Mantri Jan Dhan Yojana (PMJDY), India has not only transformed access to formal banking but has also emerged as a global leader in digital payments. 56% of these accounts are held by women. The Jan Dhan accounts became the entry point into an expanding ecosystem: once opened, they were linked to Aadhaar identity credentials and to the UPI payment rail, creating a pipeline that carried not just money but data the transaction records that, properly analysed, constitute a credit profile for hundreds of millions of people who have never had one before.

The payments dimension of this story is itself historic. In 2024, UPI processed about 172 billion transactions, up 46% from the year before, and a staggering 247 trillion rupees ($2.7 trillion) moved along this free money highway, according to the National Payments Corporation of India. For comparison, Visa's global network processed approximately 234 billion transactions in 2024. A piece of Indian public infrastructure operating at zero cost to consumers is now competing with the world's private payment giants and growing faster than both.

Pre 2010 estimates suggest that the cost of onboarding a customer in India, involving physical collection and verification of paper documents, ranged between $15 and $23 per customer. When a low income household seeks to open a savings account with a deposit equivalent to $1.20, this cost far exceeds any potential interest margin. India Stack collapsed this cost to near zero, transforming the economics of financial inclusion from a development obligation into a commercially viable proposition. The credit dimension followed: since April 2015, loans worth nearly ₹38 lakh crore have been sanctioned under the Mudra scheme, covering about 56.32 crore loan accounts. Nearly 67% of these loans have gone to women entrepreneurs.

What India demonstrates and what every emerging market policy maker and infrastructure builder should study carefully is that the path to mass credit access runs through public infrastructure investment, not through competition among private lenders. Private lenders will deploy capital efficiently once the rails exist. They will not build the rails themselves, because the returns on infrastructure investment are diffuse and long dated while the costs are immediate and concentrated. The state must build the plumbing; the market can distribute the water.

Part VI: The AI turn scoring the previously invisible

The mobile money revolution created the data. India Stack created the rails. The third wave of transformation is the emergence of AI driven credit scoring capable of reading and acting on data that traditional models cannot process.

Traditional credit scoring methods, grounded in historical repayment records and static financial ratios, are increasingly inadequate for the realities of platform based lending where borrowers often have thin or nonexistent credit files, incomes are volatile, and financial behaviors are embedded in complex digital ecosystems. The FICO model unchanged in its fundamental architecture since 1989 was built for a world of stable employment, formal credit histories, and documented income. It was not built for the gig economy worker in Lagos, the smallholder farmer in rural Bihar, or the market trader in Nairobi whose economic life is rich, active, and entirely invisible to a traditional bureau.

The alternative data available to AI driven scoring models in these markets is substantial. Alternative data integration includes telecommunications account information, e-commerce payment histories, peer to peer payment networks, geographical location indicators, and utility service management habits that together offer holistic representations of real repayment ability. Machine learning models trained on these signals rather than on the bureau data that is absent in most emerging market contexts are demonstrating predictive accuracy that rivals, and in some cohorts exceeds, the accuracy of traditional scoring models applied to populations for which they were designed.

The market is responding. The global Credit Scoring AI market size in 2024 stands at USD 2.45 billion, with a robust compound annual growth rate of 23.6% projected from 2025 to 2033. By 2033, the market is forecasted to reach an impressive USD 19.8 billion. The fastest growing region is Asia Pacific, driven by the large unbanked population, rapid digitisation, and expanding digital lending platforms. Latin America and the Middle East and Africa are next, as fintech infrastructure investment accelerates and regulatory modernisation creates space for alternative data models.

In Latin America specifically, the pattern is familiar from Africa: a large economically active population, thin bureau coverage, and a rapidly expanding mobile and digital payments substrate that is generating the data signals that AI models can read. In Latin America and India, regional data ecosystems can be harnessed to deliver tailored credit solutions to local SMEs and consumers, bridging access gaps. The BNPL explosion in Nigeria from $325 million in usage in 2022 to a projected $1.195 billion by 2028 is, in part, a story of AI driven underwriting making it possible to approve credit in seconds for consumers who would have been rejected, or never evaluated, by any traditional institution.

"The FICO score was revolutionary because it made credit assessment portable, consistent, and fast. AI driven alternative scoring is revolutionary for the same reason except it extends those benefits to the two billion people that bureau-based models have always left outside the door."

The risks are real and should not be minimised. Machine learning models are capable of encoding and amplifying biases present in their training data if the data reflects historical exclusion, the model may perpetuate it. The "black box" problem the difficulty of explaining why a specific borrower was declined creates regulatory and ethical challenges, particularly in jurisdictions with consumer protection requirements around credit decisions. And the use of behavioural data, location data, and social signals raises legitimate privacy concerns that must be addressed in system design rather than deferred to compliance.

These are challenges of implementation, not arguments against the fundamental proposition. A credit system that can see two billion people it currently cannot see, and that can assess their creditworthiness based on how they actually behave rather than on the formal records they lack, is a credit system that is fundamentally more just than the one it replaces. The obligation is to build it carefully not to decline to build it at all.

Part VII: The private credit surge and the new capital architecture

While the credit infrastructure transformation has been playing out in emerging markets, the architecture of credit in mature markets has undergone its own structural shift. The post Global Financial Crisis regulatory environment which constrained bank lending, increased capital requirements, and pushed large swathes of corporate credit into non bank channels has produced one of the most dramatic structural changes in financial history.

What was once a modest niche occupied by mezzanine funds and specialty finance companies has grown into a market with approximately $1.34 trillion in U.S. assets and nearly $2 trillion globally as of mid 2024, rivaling the broadly syndicated leveraged loan market in scale. Private credit grew from $158 billion in assets under management in 2010 to nearly $2 trillion by mid 2024 a more than thirteen fold expansion in fourteen years, at a compound annual growth rate of 22%. Total private credit has grown to be comparable to the leveraged loan market ($1.4 trillion) and high yield bond markets ($1.3 trillion).

This is not merely a cyclical phenomenon. It represents a structural repositioning of the boundary between bank and non bank credit intermediation a shift that the existing regulatory architecture was not designed to address. The emergence of private credit as a major asset class has created new channels for institutional capital to reach borrowers, and it has done so with greater flexibility, speed, and relationship depth than public markets can provide.

The implication for emerging market credit infrastructure is significant. As private credit matures as an asset class in developed markets, institutional investors pension funds, insurance companies, sovereign wealth funds are looking for yield, diversification, and access to growth that developed market credit cannot offer. The Asia Pacific private credit market is projected to grow from $59 billion in 2024 to $92 billion in 2027, representing a 16% compound annual growth rate. Private credit transactions in Asia typically offer a 300 - 400 basis point margin over U.S. equivalents. The capital appetite is present. The infrastructure to intermediate that capital into emerging market credit assets to give international investors a standardised, legible, priceable exposure to Sub Saharan African consumer credit, to South Asian SME lending, to East African agricultural finance is what is still being built.

This is the connection between the private credit revolution in mature markets and the credit infrastructure work underway in emerging ones: the former has created the demand, and the latter is building the supply. When the infrastructure exists to package local credit risk into standardised instruments that institutional capital can price and purchase, the channel will open. The demand is there. The question is whether the plumbing can be built fast enough to meet it.

Part VIII: What the arc tells us and what comes next

Five thousand years of credit history reveal a pattern that repeats across every era: the expansion of credit has always followed the expansion of information. Mesopotamian priests could lend to farmers because they knew which farmers had produced grain before. Italian bankers could extend letters of credit across Europe because they had networks of agents who vouched for merchant reputations. FICO scores enabled mass consumer credit because they made borrower history legible at scale across an entire national population.

Every expansion of creditworthy information has produced an expansion of credit access. And every moment of information scarcity every period when the relevant data existed but could not be read, assembled, or transmitted to those who needed it has meant that creditworthy people were denied credit not because they were untrustworthy but because the system could not see them.

That is precisely the situation in most of the world today. The data exists. Mobile money transaction records, utility payments, agricultural purchase histories, digital commerce patterns these are rich, recent, and predictive. The gap is not in the data. It is in the infrastructure that would allow that data to be assembled, verified, anchored to a portable identity, processed through models calibrated to local behaviour, and delivered to institutions in a form they can act on.

The switch to digital payments offers opportunities to offer funding to small businesses, which often struggle to access credit. In particular, digital transaction records can help small scale merchants demonstrate cash flows to secure loans, bringing funding opportunities to those who lack traditional credit histories. The World Bank's Global Findex puts the point bluntly: the formal credit gap is not primarily a problem of demand or creditworthiness. It is a problem of legibility of the system's inability to read the economic lives of the people it should be serving.

The evolution of credit is not complete. It has been, for five millennia, a story of progressively better information enabling progressively wider access. The current moment the convergence of mobile data substrates, AI driven scoring models, self sovereign identity infrastructure, and institutional capital seeking emerging market exposure represents the most significant expansion of that information frontier since the introduction of the credit bureau in the mid twentieth century.

The Sumerian farmer who borrowed grain from the temple and repaid it after harvest was doing something recognisable as credit. The Kenyan market trader whose M-Pesa transaction history is, for the first time, being read by a machine learning model and translated into a loan approval she is doing the same thing. Five thousand years apart, both are navigating the same fundamental transaction: the exchange of present value for future obligation, grounded in a system's confidence that the borrower is trustworthy.

The difference is that the system is finally, slowly, learning to see her.

The Weritas view

At Weritas, we read this history not as background but as design brief. The arc of credit's evolution points clearly toward where the next infrastructure must be built: at the intersection of portable digital identity, alternative data processing, AI driven risk assessment, and standardised credit instruments that can move international capital to local credit risk.

The WERI ecosystem is our attempt to instantiate that intersection to build, for the credit markets of Sub Saharan Africa and beyond, the equivalent of what the Medici network built for medieval Europe, what FICO built for post war America, and what India Stack is building for the twenty first century's most populous democracy: a layer of shared infrastructure on which a new era of credit access can be founded.

The history suggests we are not early. We are, if anything, late. The data substrates are maturing. The AI models are ready. The capital is looking for a home. The regulatory frameworks are crystallising. What remains is the will to build the infrastructure that connects them openly, responsibly, and at the scale that the moment demands.

| $2T | $1.1T | 172B |

| Global private credit assets under management by mid 2024, up from $158B in 2010 | Mobile money transactions processed across Sub Saharan Africa in 2024 alone | UPI transactions processed in India in 2024, up 46% year on year |

| 530M | 75% | $19.8B |

| Jan Dhan bank accounts opened in India, the world's largest financial inclusion programme | Adults in low and middle income economies with a financial account in 2024, up from 42% in 2011 | Projected global AI credit scoring market by 2033, up from $2.45B in 2024 |

This perspective represents the views of the Weritas research team. It does not constitute investment advice or a solicitation of investment. For institutional and partnership enquiries: partners@weritas.io · www.weritas.io